If you are like my clients, your family, personal time and career are your top priorities. Taking time away from them to talk about insurance or saving for the future seems as much fun as going to the dentist. However, you spend time to maintain your health with annual checkups, maintenance on your house and car - but do you spend as much time to keep on top of your financial security?

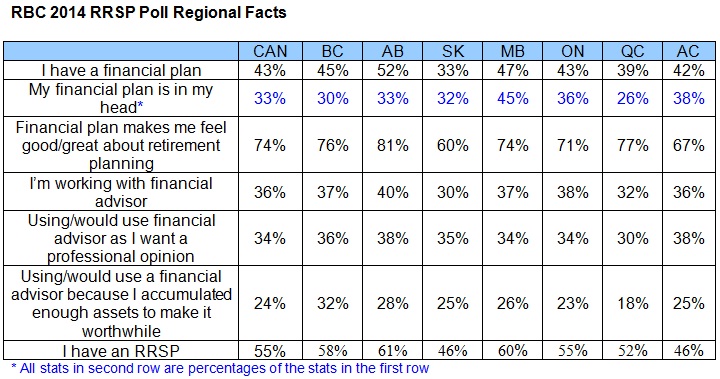

Fully 66% of Canadians report that they do not have a written financial plan. Only 36% are working with a financial advisor1.

Why do most people neglect their financial planning? Some of the top rationalizations include:

- I’ll save for retirement when I make more money.

- There are so many options out there; it’s too overwhelming to begin.

- It’s too expensive.

- I have great benefits through work.

- I have more than enough savings and insurance.

- I don’t have time. There is always tomorrow.

Do any of these sound familiar?

If you are like my clients, you are probably also lacking information and resources to help you make the best decisions to protect your family and your income.

I’m here to provide the information and resources you need to make those decisions. Because I prefer for the process to be simple and uncomplicated, I break it down into 3 areas. We’ll have meaningful conversations about what happens if:

- You live too long

- You die too young

- You get sick or injured

You live too long

This means you have outlived your savings. It’s no secret we are all living longer but many are not prepared or aware of the cost associated with this: inflation, changing government pensions, from living an active life style in retirement to planning for the likely associated medical and heath cost there will be. You have to turn to others, private or public, for financial assistance in your final years of life. There are ways to plan for this and to ensure that your money lasts so you will be able to live independent and on your terms.

You die too young

This means you have left your family, spouse or children without your support - financial or otherwise. Whether you are a one income or two income home, each person contributes in very real ways that would mean a financial loss on top of the emotional loss of a loved one.

The biggest question is not “Do I need?” but “How much do I need?”

There is a big difference between price and cost. Which one of these do you use to base your decisions? Each situation is different, and I will work with you to determine the best answer to that question as it evolves over time. How to integrate existing employee benefits into the equation. There are many options, regardless of your budget.

You get sick or injured

This means losing your income. Whether it is a car accident or cancer, your risk of losing your income is bigger than you think. Will you be able to pay your bills without depleting your savings? Will medical expenses cut into retirement options?

- What happens when I have a claim?

- What information will my existing insurance carrier need at that time?

- Will it do what I believe it will do and if so how long for and how long will they pay?

- What will the government pay for? What are their exclusions?

- If I make a claim, will the government change what they will pay for in the future for other illnesses, accidents or unplanned events?

We will take a look at your exposure and determine the best way to help you ensure that a loss of income – temporary or permanent – will not mean losing your quality of life.

Here is how a couple of my clients have described their experience working with me:

First steps

I first met Thomas a couple of years ago after a friend of mine introduced us. After we met there was no immediate need to make any changes or add anything new with regards to our insurance portfolio, however I understood it would only be a matter of time until that situation changed. Thomas kept in touch on a regular basis and in a professional manner? I never felt pressured or uncomfortable. Recently, it was time to make changes (update our insurance coverage, look into new products to cover a wide range of coverage, and our existing advisor was leaving the industry). Thomas stepped up to bat. He validated everything we had, kept what was still good and relevant as well as reassessing our needs so we were then able to prioritize the changes we needed to make. We took care of the biggest areas of risk, and will take care of the other areas over time. Thomas made the process of addressing our insurance needs simple, easily, and thoroughly. If there are any challenges along the way he will find the answers to get the best possible outcome. Highly recommended.

Thorough, Diligent, Knowledgeable & Informative

I have entrusted Thomas to handle my insurance needs. What I find in Thomas is an individual who genuinely cares about your specific situation and will go above and beyond to obtain the best scenario to suit your needs. I was not overly familiar about insurance and what is required, recommended or safe to have as coverage, however Thomas did an amazing job at informing me of my needs and what is best for me. I definitely appreciated that he kept me informed throughout the entire application process and went out of his way to present me with the final paperwork once my policy was issued. I feel protected having Thomas as my agent / advisor. Even so, that I’ve asked Thomas to take over an existing policy that I had in place. I recommend Thomas Thorne with 5 stars!

To see what other clients have said about me go to our testimonial page.